I have written before about how my days of leverage trading turned into a complete disaster. Those days are, in fact, the reason I am sitting here now playing with agentic AI, back writing software for clients, rather than kicking it up somewhere in the Caribbean. That blow-up taught me the only lesson that ever really mattered: a position you cannot hold through being wrong is not a conviction, it is a time bomb. So everything I am about to describe is unleveraged, holdable, and survivable. I learned that part the hard way.

But here is the thing I have been avoiding.

My long-term thesis on the world was reasonable. In some respects it was exceptional. And I have not revisited it in about four years.

I have not stress-tested it. I have not gone back and asked whether the conditions that made it true are still the conditions I am living in. I just formed it, let it run, and watched it mostly play out the way I expected. Which is exactly the trap. A thesis you formed four years ago and never looked at again is not conviction anymore. It is inertia wearing conviction’s coat. My life has changed beyond recognition in those four years. It would be strange if my read on the world did not need at least a service.

So this is me, doing it in public, in real time. Not presenting a finished answer. Working it out on the page.

Tracing it backwards

It is very hard to describe how a position evolved going forwards. It is much easier to state where you ended up and then work out how you got there. So let me trace it back.

Where I landed was this. I decided, in the end, that fine-grained indicators are mostly noise, subject to so much compounding error that they are worse than useless. You need something simpler and directional. So I built my read around a small number of large forces, and I held it loosely enough to be directional rather than precise.

There were three layers to it.

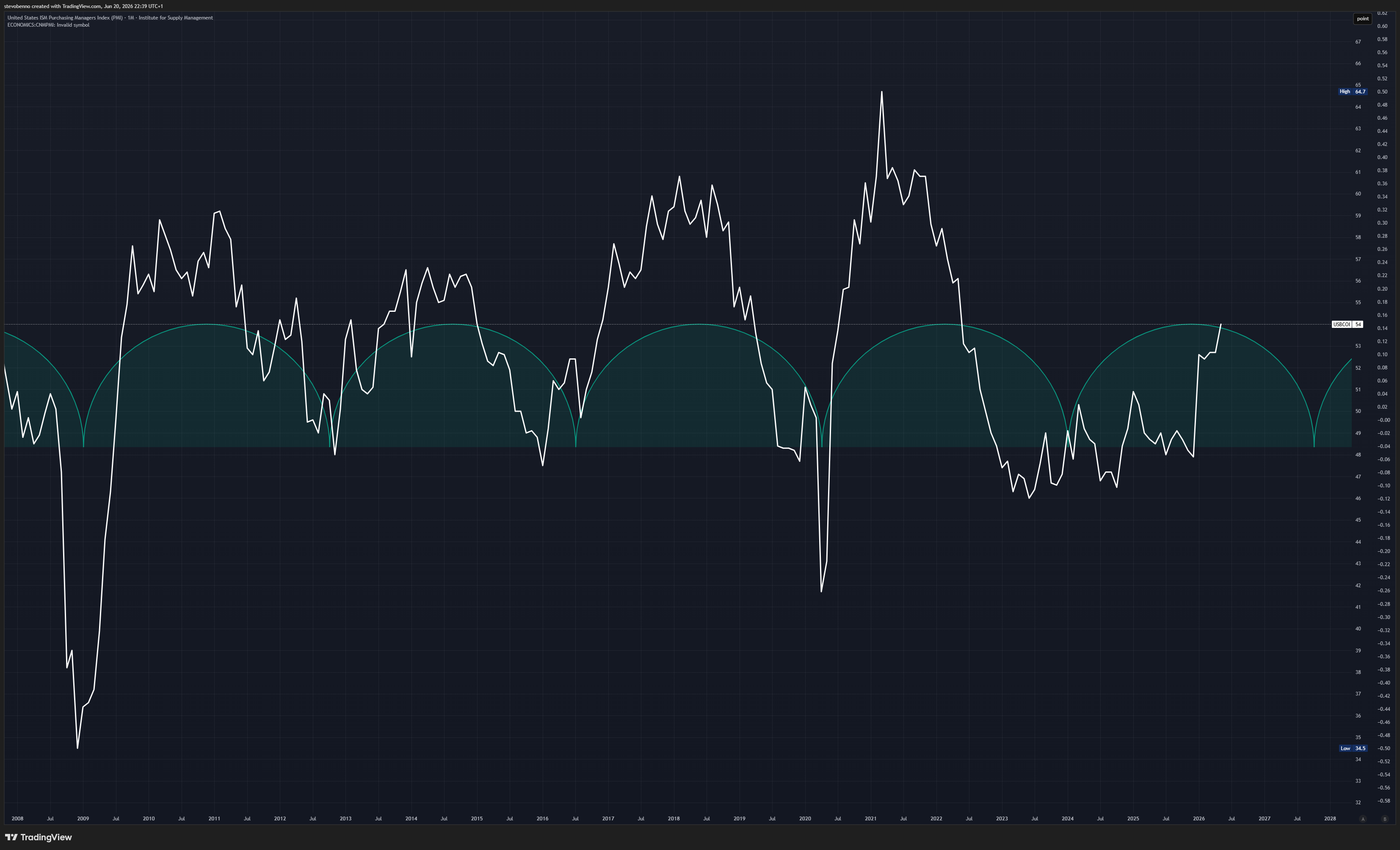

The first was timing. After 2008, the world went into what I think of as a kick-the-can cycle. I had read somewhere that vast quantities of national debt need refinancing every few years, and because of that, the business cycle, as you can see it in something like the Purchasing Managers’ Index, stopped being random and started bobbling along in regular little molehills. Predictable rises and falls. That gave me a rough clock. Not direction on its own, just a sense of when to expect the market to amplify a move. Near the top of a molehill, expect more upside. In a trough, expect less, or a fall. Nothing precise. Just a rhythm.

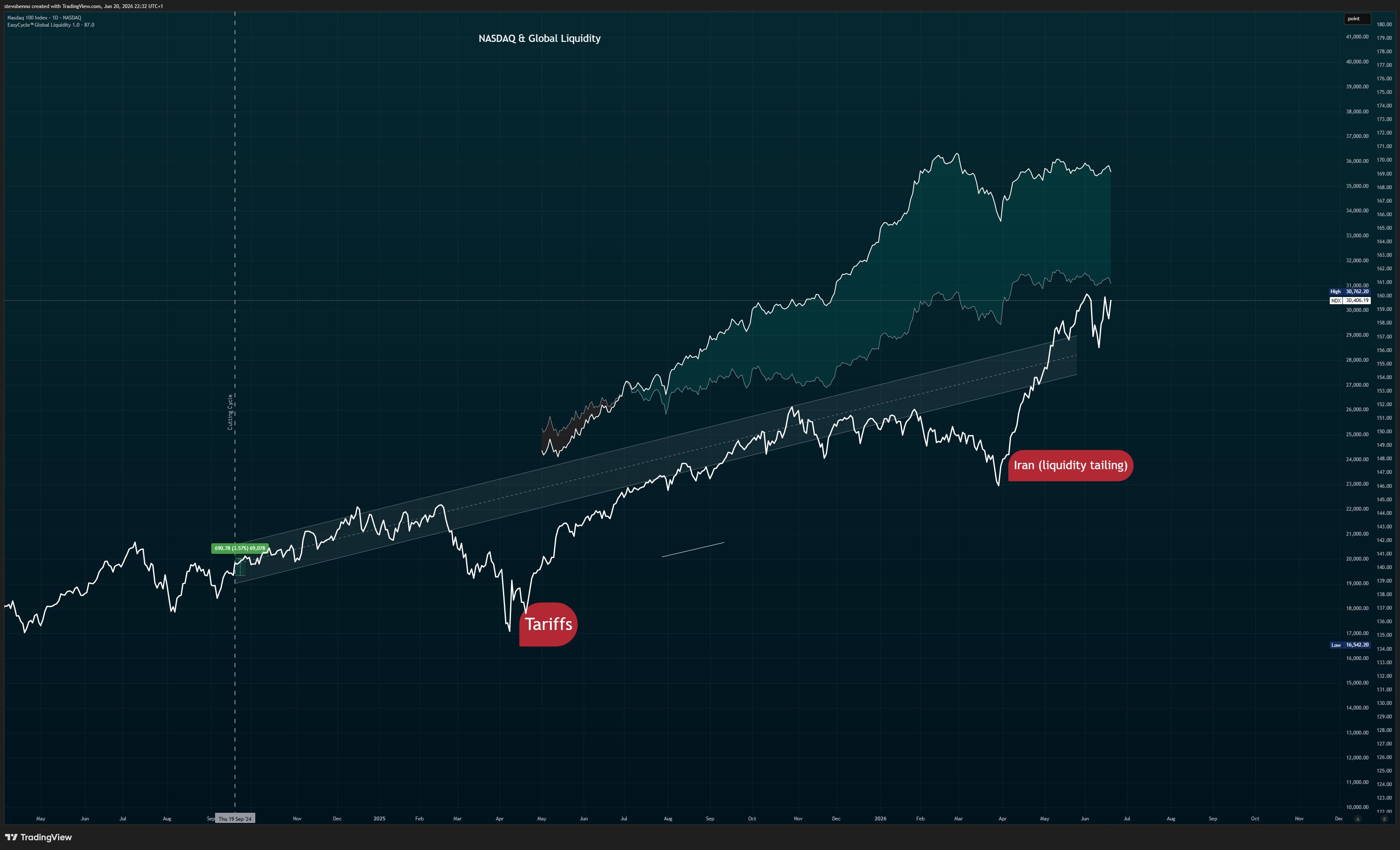

The second layer, and the real engine, was global liquidity. When there is more money in the system, it has to go somewhere, and it pushes assets up. When liquidity contracts, the tide goes out. I did not invent this. I am not that clever. I more or less stole the work of Michael Howell at CrossBorder Capital, whom I had watched talk many times and admired, and I tried as hard as I could to emulate his calculations and build something that looked roughly similar from the public data I could get my hands on. To this day, that liquidity model is still my primary driver of direction.

The third layer was the clever one, and it is the part that stops the whole thing being naive. Liquidity on its own would have told me, in March 2020, that markets should rise, because the world was being flooded with stimulus. But markets crashed first. The model has to account for that. Liquidity is necessary, but it does not reach the assets while fear and panic and uncertainty are high. The cash sits there, dammed up, while markets fall despite it. Then, as the panic resolves and a sense of predictable calm returns, the dammed-up liquidity floods in and markets explode upward. So the real signal was never liquidity on its own. It was liquidity adjusted for volatility. COVID was the clean proof of it. I have watched it again more recently with Trump and his tariffs: tariffs land, the world turns uncertain, markets tank, but the liquidity-adjusted reading says steady as she goes, and the recovery arrives almost exactly on cue.

That is the machine. A clock, an engine, and a damper. And for four years it has mostly worked.

The part I absorbed rather than worked out

Here is where I have to be honest with myself, because the machine I have just described is neutral. Liquidity up, assets up. Liquidity down, assets down. It oscillates. It does not, on its own, tell you to be long and to stay long.

So why did I end up long, and holding?

Because underneath the machine there is a worldview, and I need to own where I got it. I went down the rabbit hole. The Bitcoin Standard, then von Mises, then Hayek, then Friedman, and then, God help me, I read Ayn Rand’s novels. All of them. For a while there I was a fully paid-up, hyphenated member of the libertarian-adjacent objectivist society. It was never the cleverest position in the world, and I have walked a good distance back from it since.

But here is what I will not do, because it is the lazy move in the other direction: I will not now pretend that because I absorbed a thesis as something close to a convert, the thesis is therefore wrong. Those are independent things. You can arrive at a true idea through a motivated, oversold pipeline. The pipeline oversells it. That does not make it false.

And the core of it is, I think, still true. It is the idea that fiat money is structurally biased toward debasement. Not because of a conspiracy, but because of incentives. Any institution that is only elected for five years will kick the can down the road, because can-kicking means deferring the hard, painful, unpopular decisions and appeasing whoever is loudest now. So deficits grow. The people at the top mostly know it is unsustainable, and mostly seem to be praying for some kind of miracle, which I suspect increasingly has the words “artificial intelligence” in it. But that is for another day. The point is that, barring something extraordinary, the long-run direction of liquidity is expansion. There may be periods of contraction along the way, but the bias is up.

You only have to look at how the world is actually playing out. Look at the state we have left young people in, mortgaged to the hilt to pay for a present they did not vote for. That is not ideology. That is the mechanism, visible in the data.

Can it go on forever? No. I read somewhere that the vast majority of fiat currencies in history have eventually gone to zero, and that the dollar has lost something like nine-tenths of its purchasing power in a century. I should say plainly that I first picked those figures up from Michael Saylor in my disciple days, and a stat you inherited from an evangelist is exactly the kind you should re-check before you lean on it, so treat them as directional until I have verified them properly. The direction, though, is not really in dispute. Money debases. The argument is only about pace.

So that is the thesis, traced back and laid bare. A neutral liquidity machine, pointed permanently upward by a debasement worldview I absorbed during a period of my life I now see more clearly. And for four years I have let it run without once asking whether the world it was built for is the world I am still in.

The fractures

When I actually turn the lens on it, I find three places where the thesis might be expiring, and they do not all point the same way. That is what makes this interesting rather than comforting.

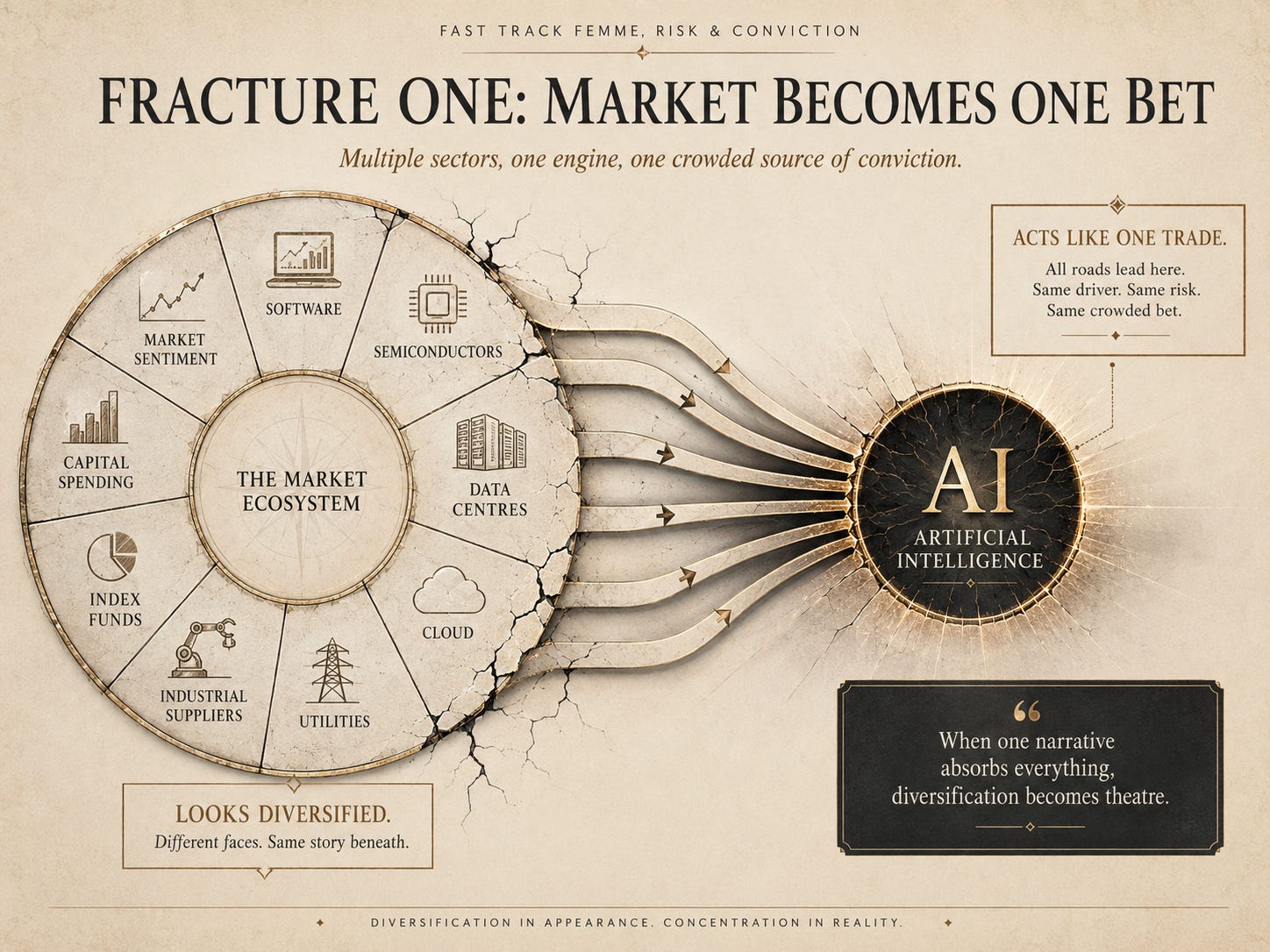

Fracture one: the market has become a single bet

My liquidity model has no term in it for concentration. It assumes that if liquidity flows, it flows into “the market,” as if the market were a broad, diversified thing. It is no longer a broad, diversified thing.

As I write this, in June 2026, the Magnificent Seven are around 35 percent of the entire US market by value, up from about 12 percent a decade ago. In 2025, roughly 42 percent of the S&P 500’s total return came from those same seven companies. The top ten companies are about 38 percent of the index’s value and around 31 percent of its earnings, and by some measures the Mag Seven generate close to 70 percent of the economic profit of the whole index.

It gets starker when you look at the real economy rather than the market. By one Harvard estimate, data-center investment accounted for around 92 percent of US GDP growth in the first half of 2025, while being only about 4 percent of GDP. Strip out the AI infrastructure build, on that reading, and growth would have been roughly nothing. Other estimates are less extreme but tell the same story: AI infrastructure contributing something like half of all GDP growth, and a serious strategist or two suggesting that without it the economy might already be in recession.

So here is the problem the liquidity model cannot see. The entire market, and increasingly the entire economy, is leaning on one sector. A model that says “liquidity up, markets up” is blind to the possibility that the market has quietly become a single, concentrated bet, so that a real or even imagined wobble in that one sector cascades through everything regardless of what liquidity is doing. Liquidity can be ample and the thing can still fall fifty percent if the load-bearing wall cracks. I wrote yesterday about the eye-watering value being put on certain private AI-adjacent names. If one of those re-rates hard, the contagion does not care how much money is sloshing about.

This is the downside fracture. It is not in my model, and it is at a historic extreme.

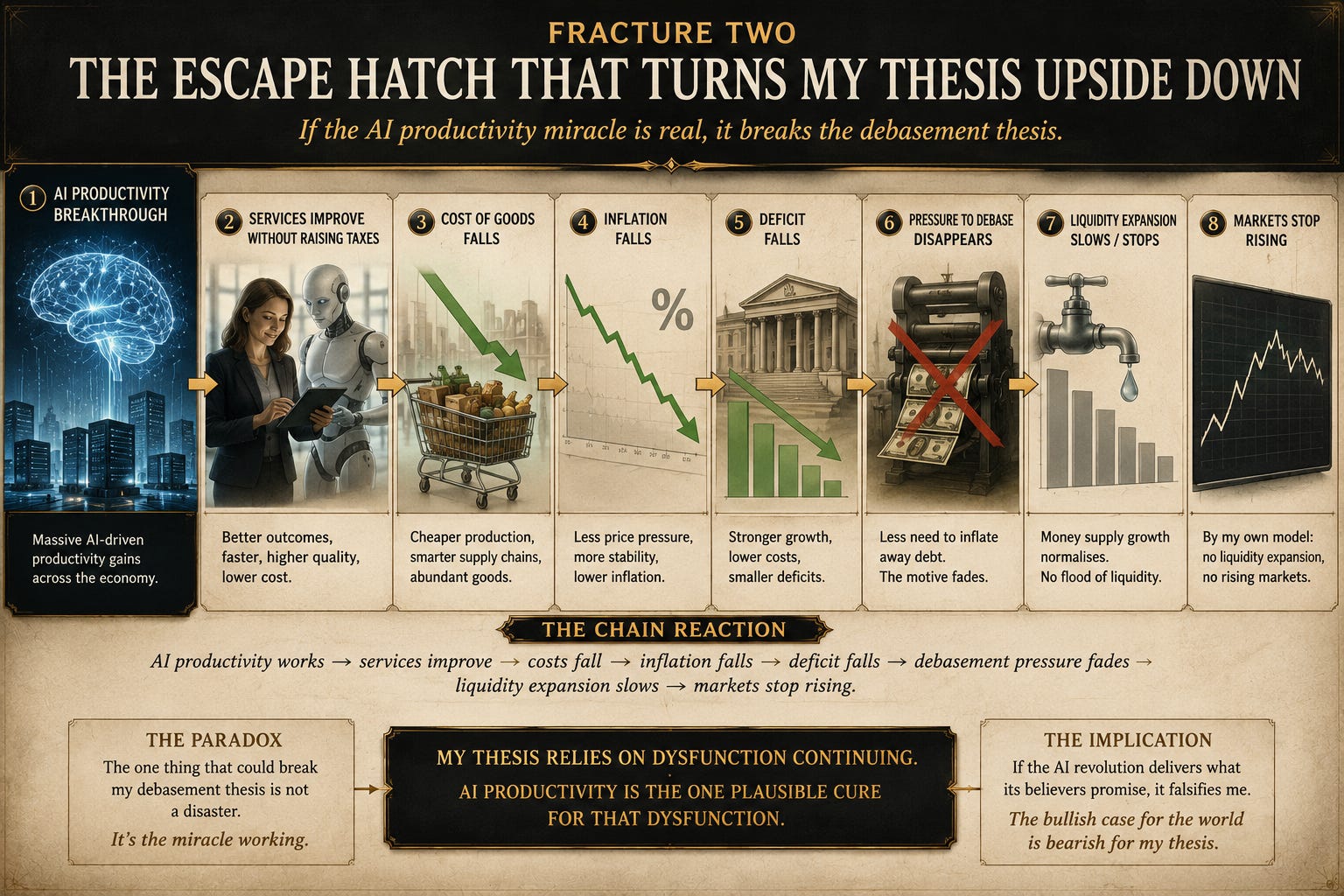

Fracture two: the escape hatch that turns my thesis upside down

The second fracture is stranger, because it is the bullish case for the world, and it is bearish for my thesis.

Suppose the AI productivity story is real. Suppose it delivers genuine, double-digit national productivity gains. Then follow the chain. Services improve without raising taxes. The cost of goods falls. Inflation falls. The deficit falls. And if the deficit falls, the structural pressure to debase, the very thing my whole directional bias rests on, goes away. Liquidity stops needing to expand. And by my own model, if liquidity stops expanding, markets can stop rising.

In other words, the one thing that could break my debasement thesis is not a disaster. It is the miracle working. The thesis is, at heart, a bet on dysfunction continuing. AI productivity is the one plausible cure for that dysfunction. Which leaves me in the slightly absurd position of running an investment thesis that bets against the very thing I now stake my professional life on. If the AI revolution does what its believers say, it falsifies me.

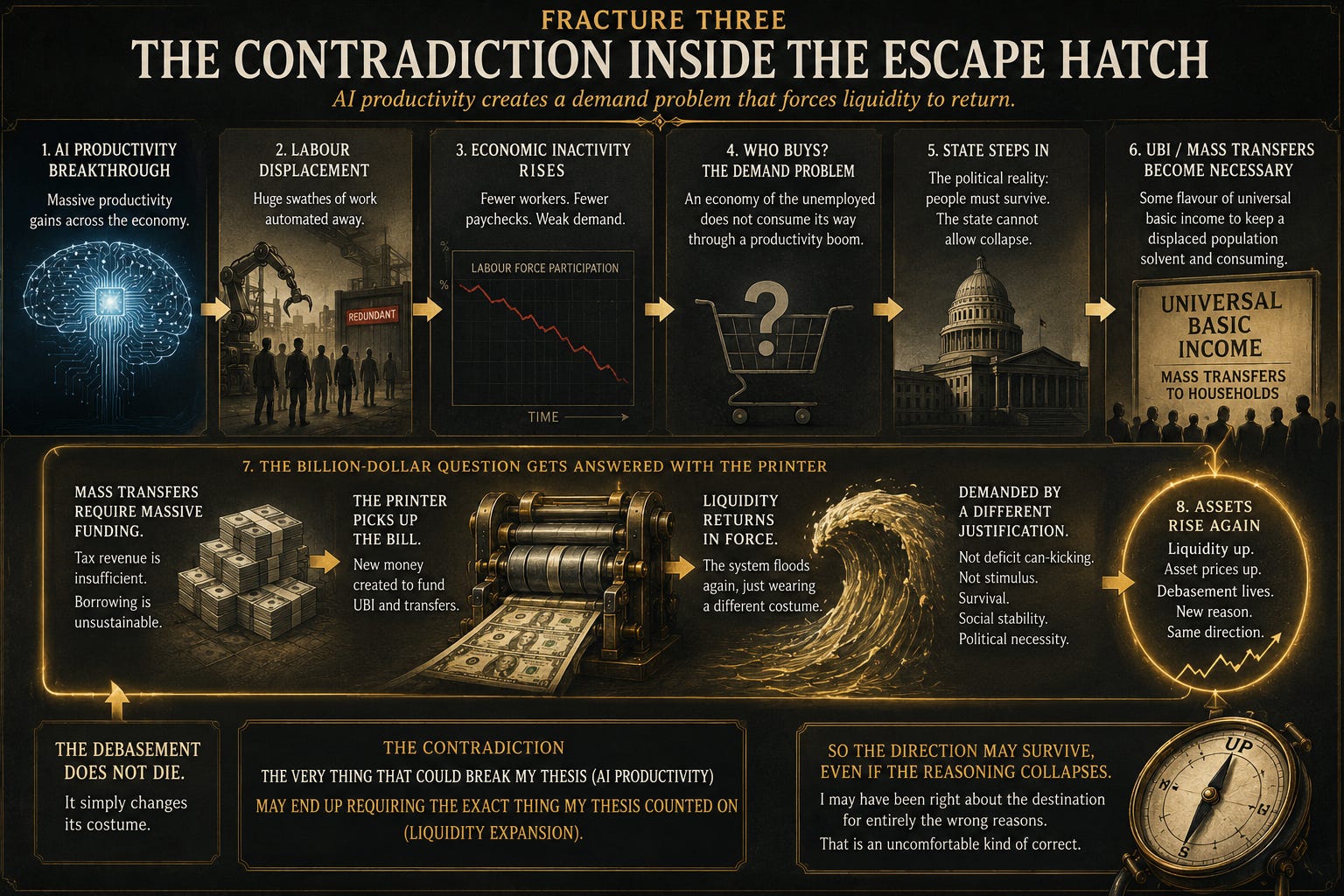

Fracture three: the contradiction inside the escape hatch

Except the escape hatch has a hole in it, and finding the hole half-rescues the original thesis from the other side.

Double-digit national productivity from AI does not arrive without enormous labour displacement. And if great swathes of people are displaced, you run straight into a question the productivity story never answers: who is buying all these cheaper, better goods and services? An economy of the unemployed does not consume its way through a productivity boom. Data centers, famously, employ almost no one once they are built. The capex props up GDP without creating the wage-earning consumer base that GDP ultimately depends on.

So what happens? The state steps in. You inherit a colossal social bill, some flavour of universal basic income, to keep a displaced population solvent and consuming. And that means the liquidity comes roaring back, just wearing a different costume. Not deficit-financed can-kicking this time, but mass transfers funded by the printer because the alternative is destitution. The debasement does not die. It simply changes its justification.

Which means the direction of my thesis, up, might be more robust than the reasoning that got me there. I may have been right about the destination for entirely the wrong reasons, and the destination may survive even as those reasons collapse. That is an uncomfortable kind of correct.

I have very strong feelings about UBI, by the way, and almost none of them are warm. But that is a whole essay of its own, and I am not going to let it hijack this one. Another time.

What this is really about

There is a political reading that sits underneath all of this, and I will keep it to an aside because it is symptom, not cause. As ordinary people get squeezed harder, they go to the extremes, left and right alike. I called this ten years ago, and you can see it now in the rise of Reform and the Greens in the UK. I suspect both will get their turn in or near government, and I suspect it will not make a blind bit of difference, because the problems are structural and far too big for either of them. That matters to my thesis only because political extremism is evidence that the pressure behind the debasement ratchet is intensifying, not resolving. The populists, whoever they are, will spend more, not less.

So where does that leave me?

The engine still works. Liquidity adjusted for volatility still describes how money moves into assets, and I see no reason to doubt the plumbing. The direction, up, still lives today. I genuinely cannot name its end date, and I am not going to pretend I can. But the reasoning I bolted underneath that direction was absorbed during a chapter of my life I now read differently, and there are at least three things my four-year-old model simply cannot price: a concentration so extreme that the market has become one bet, a productivity shock that could cure the dysfunction I am betting against, and the contradiction inside that shock that might quietly reinstall the same upward bias under a new name.

And there is one more thing the model cannot handle, which is the speed of all this. My whole timing layer assumes a stately rhythm, the gentle molehills of a slower world. An exponential change does not respect that rhythm. We are, all of us, terrible at feeling exponential change before it arrives. A thesis calibrated to the slow world has no machinery for a fast one.

So the honest position is not “I was wrong.” It is narrower and more useful than that. I was directionally right for the regime I formed the thesis in. I can no longer assume that regime is the one I am now standing in.

I saw a recent calculation that AI would have to replace about 27% of jobs in the US just to pay interest on the debt already issued, so there's definitely going to be either a crash or a revolution. I'm hoping for the crash; I don't want to love through a revolution.

Thanks for sharing your thoughts on this - I appreciate you sharing how you arrived at your conclusions.