Like everybody else this last couple of weeks, I’ve looked at the SpaceX IPO from the side of the road. And I’ll be honest with you, there was a little feeling at the back of my mind the whole time. The one that says: are you one hundred percent sure you have absolutely no interest in this? Are you certain you’re not about to watch the greatest wealth-creation event of the decade sail past you while you stand there with your arms folded, being clever?

I know that feeling well. It’s not insight. It’s the crowd’s tug. It’s the motion of the herd starting to foam and froth at the mouth at the idea of spectacular returns, and it pulls at you precisely because everyone around you is leaning the same way. The analysts queue up to tell you what Google did. What Amazon did. What you’d have made if you’d bought Nvidia in 2015 and gone to sleep for a decade. The pull is real and I felt it.

But I had a separate take. I wouldn’t claim it’s the most original take in the world. It’s just mine, and this is what it is.

The value was extracted before it ever came near me.

Let me show you what I mean, because this isn’t a feeling, it’s an arithmetic.

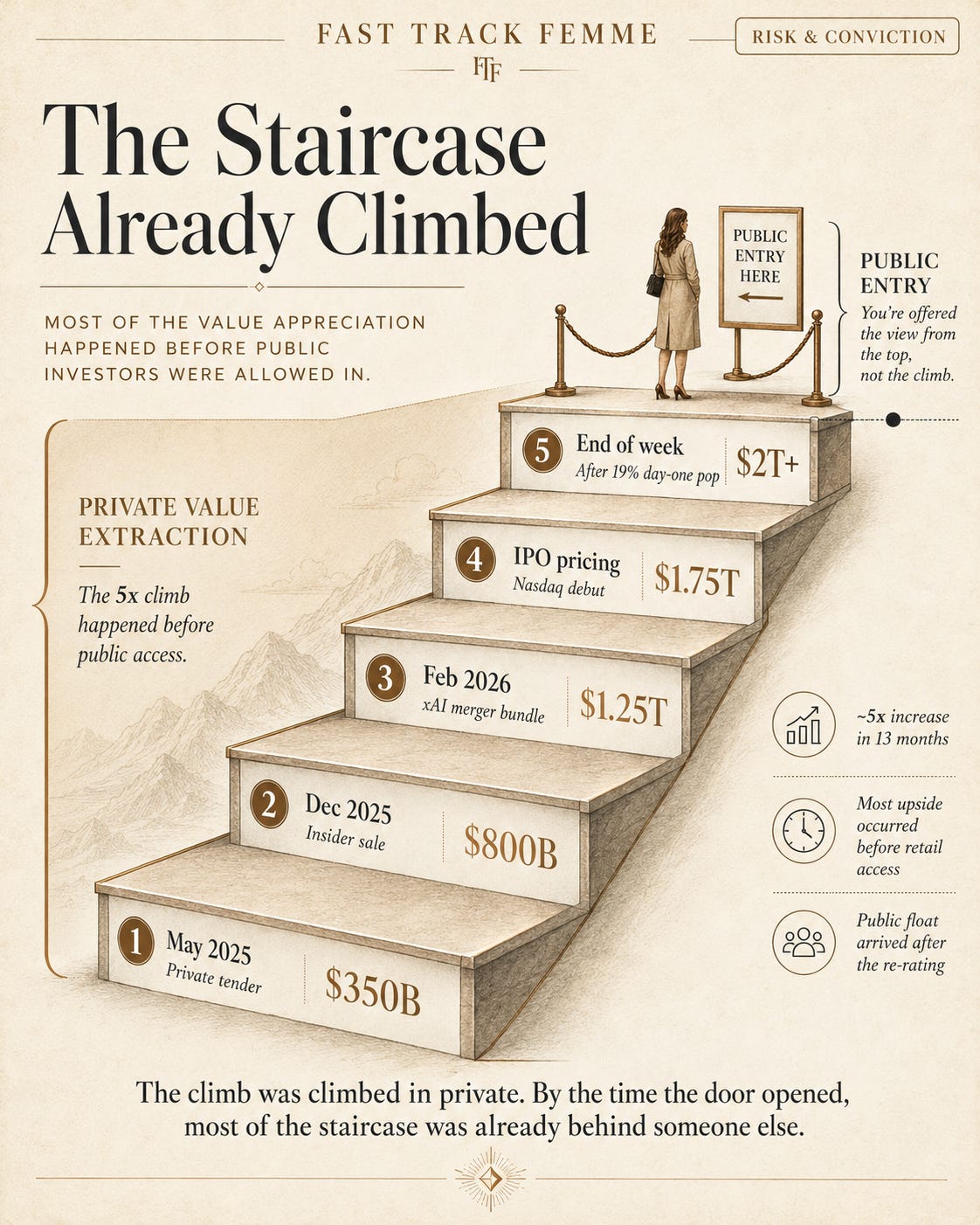

In May of last year, a private tender valued SpaceX at around three hundred and fifty billion dollars. By December, an insider sale put it near eight hundred billion. In February, the xAI merger bundled the whole thing up at one and a quarter trillion. And when it finally walked onto the Nasdaq two days ago, it priced at a valuation of one and three quarter trillion, popped nineteen percent on day one, and closed the week worth somewhere north of two trillion dollars.

So the journey from three hundred and fifty billion to one and three quarter trillion, a five-fold increase, happened entirely in private hands over thirteen months. By the time you and I were allowed to put a hand up, the staircase had already been climbed. We weren’t being offered the climb. We were being offered the view from the top, and asked to pay for the privilege of standing there.

And then I realised what it actually reminded me of. Not a shitcoin in the fraudulent sense. SpaceX is not a fraud. Starlink is real, the rockets are real. But the mechanics of the launch, the plumbing, were borrowed wholesale from the world of crypto token launches, and once I saw it I couldn’t unsee it. Three things in particular.

Vesting - A classic shitcoin move

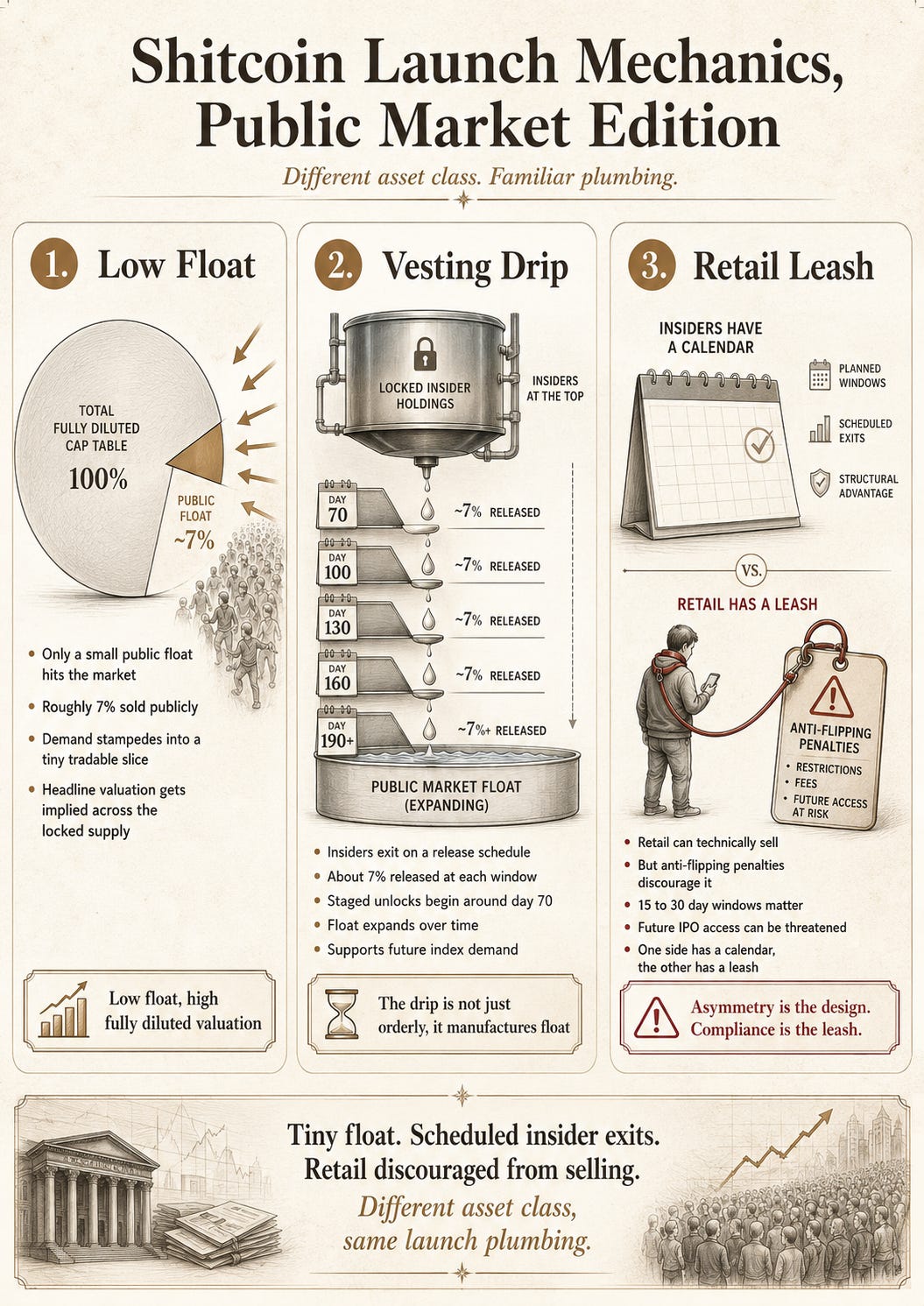

The first is vesting. In a token launch, the people with access don’t get all their coins on day one. They get a small slice unlocked at the start, and then a vesting schedule drips the rest out over months or years, on a calendar. SpaceX did exactly this. It didn’t use the normal single lockup that lifts after six months. It built a tiered release where insiders can sell seven percent of their holdings at each of a series of dates, starting around seventy days in and laddering out from there. And here is the tell. That structure was not built to protect people like me. It was engineered to expand the public float fast enough to maximise the company’s weighting in the Nasdaq index, which in turn forces index funds to buy the stock whether they want to or not. The drip is not a safety feature. It’s a demand-manufacturing machine.

Super Low Float - THE classic shitcoin move

The second is the low float. In crypto they call it low float, high fully-diluted-valuation. You release a tiny fraction of the supply, you let a stampede of demand crash into that tiny fraction, and the price that results gets multiplied across all the locked tokens nobody can sell yet, to print an enormous headline valuation. SpaceX sold roughly seven percent. It was oversubscribed by more than four hundred percent. A tiny slice against a wall of demand. That is the low-float playbook, executed at the largest scale in the history of public markets.

Retail Lock In

The third is the one that genuinely made me sit up, because it’s the one that gives the game away. The selling restrictions. I’d half-remembered that retail couldn’t just freely sell, and I went and checked, and it’s worse than I thought, though not in the way I assumed. Retail could technically sell on the open market. But the brokers handing out the shares attached anti-flipping penalties to them. Sell your Fidelity allocation inside fifteen days and you can be locked out of future IPOs. SoFi runs a thirty-day window and escalates to a permanent ban for repeat offenders, and will charge you fifty quid for the privilege. And the threat with teeth is that flipping your SpaceX shares could cost you your allocation in the OpenAI and Anthropic floats still to come. So picture the asymmetry. The insiders have a vesting calendar that lets them sell on schedule into the demand. The retail buyer is threatened with exile for trying to take profit in the same window. One side has a structured exit. The other side has a leash.

And then, underneath all of it, the part almost nobody is talking about. A large chunk of SpaceX shares are held through special-purpose vehicles, stacked two and three tiers deep. When the lockup lifts for the top-layer vehicle, it has thirty days to pass shares down to its investors, who then pass them down again. The people at the bottom of that stack won’t even know what they truly hold until months after the public calendar says it’s done, and they’re exposed to hidden fees and delays along the way. If you have ever watched a token launch unwind, you know exactly what that shape is. It’s the tiered bagholder. The further down the stack you sit, the later you find out what you’re actually holding, and the more of it has already been decided above your head.

That was the moment the feeling became a conviction. None of this is illegal. None of it is even unusual any more. But it is borrowed, beat for beat, from a world I watched eat retail alive only a few years ago. Tiny float. Vesting drip. Restricted exits for the little guy and scheduled exits for the big one. I have seen this film. I know how it ends for the person who shows up late and excited.

There’s one more thing in the parcel worth naming, because it’s the bit that stops you valuing the thing cleanly even if you wanted to. You cannot buy SpaceX. You think you can, but you can’t. What you can buy is a bundle. Inside it is Starlink, a genuinely excellent business and the only profitable segment in the whole enterprise. Inside it is the rocket company, extraordinary and lumpy and hard to value. And stapled on in February at a quarter of a trillion dollars is xAI. Grok. The former Twitter. A money-incinerating AI operation that, in 2025, contributed about three billion in revenue while burning roughly fourteen billion in cash, consuming more cash by itself than every other part of SpaceX generates. The combined company turned a tidy profit in 2024 into a five billion dollar loss in 2025, and the entire swing is xAI. So you can’t price the rocket cleanly, you can’t buy the satellite business on its own, and the whole thing has to be swallowed as one act of faith. That isn’t an accident of how the company grew. That’s the package, as designed.

Now, in fairness, the bulls aren’t fools and I’m not going to pretend they are. The serious independent valuations put fair value well below where it’s trading, somewhere around a third of today’s price, and the bull case openly admits this is three moonshots in one company that only works if most of them land. You can read those numbers for yourself. I won’t labour them, because they’re not actually what decides it for me.

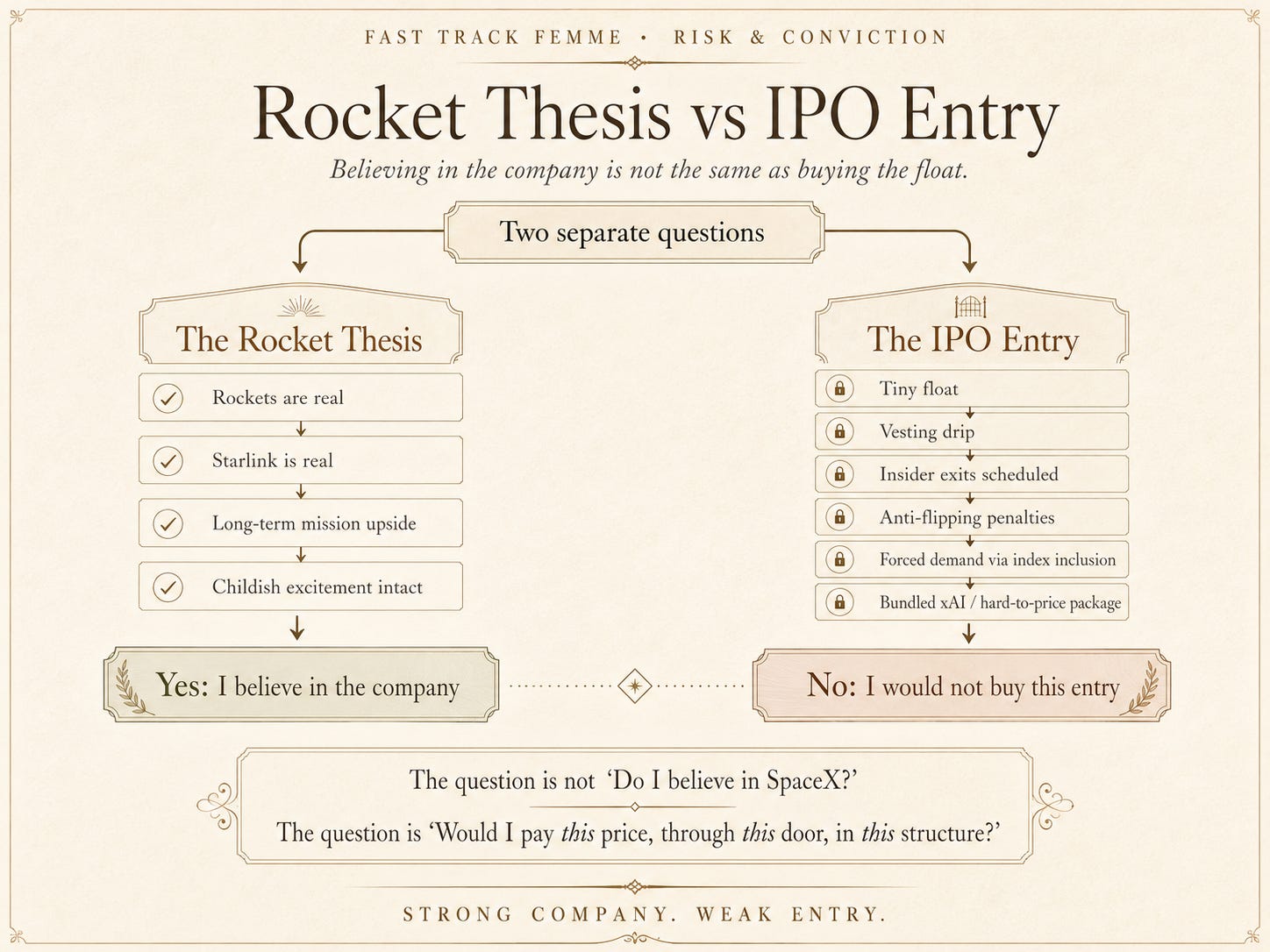

What decides it for me is simpler, and it’s two separate questions that everyone insists on collapsing into one.

Do I believe in the rocket company, as a rocket company? God, yes. Completely. I want him to do this. I am genuinely, childishly excited to see whether he can put data centres in orbit, whether Starship becomes routine, whether the whole improbable thing works. If you’re asking me whether I believe in SpaceX, I’m in the front row, cheering.

But that is not the question the IPO is asking me. The IPO isn’t asking do you believe in the rockets. It’s asking will you pay this price, today, for a bundle, through this structure, where the float is a sliver, the insiders have a vesting calendar, and you’ve been threatened with exile for selling too soon. And to that question, the answer is just as clear, and it isn’t about the rockets at all.

I thought he was launching rockets. And he is, genuinely, gloriously. It’s just that the IPO around them was a shitcoin launch with rocket boosters attached.