Why I’m Going Off MicroStrategy

Not entirely. Not angrily. But the trade has changed, and clean Bitcoin exposure now looks better for the middle case.

A small warning before we begin: this one is not my usual sort of essay.

If you have read much of my writing, you will know I usually write about transition, grief, family, identity, reinvention, and the general circus of trying to become yourself while everyone else has an opinion about it.

This piece is about investing, Bitcoin, MicroStrategy, European regulation, and the slightly absurd question of what to do next with a trade that worked far better than it had any right to.

I have pitched it at the level I understand it myself. That may mean some readers find it too technical, and some finance people find it insufficiently dressed up in expensive nonsense. I am fine with both outcomes.

The point is not to offer investment advice. It is to think out loud about conviction, risk, changing your mind, and the moment when the instrument that once expressed your thesis cleanly becomes more complicated than the thesis itself.

If that is not your thing, I entirely understand. I will be back to emotional devastation, jokes about facial surgery, and transgender life in rural Ireland shortly.

I used to write Pine Script algorithms. Not the simple kind that draws moving averages on a chart and calls it a system, with two shitty little EMAs and a bit of colouring in (CTO Larrson, you know who you are. A thousand quid you charge for that piece of shit I could code in 4 minutes) .The deranged kind. Liquidity models driven by bond volatility, technical overlays cascaded through three timeframes, custom indicators feeding custom indicators, a trading rig that looked like the cockpit of something NASA would politely decline to launch.

I had API adapters I’d written in C# for Bybit and Binance because the platform UIs would not execute the kind of cascading trailing stops I wanted. I was running synthetic spread trades between MicroStrategy and Tesla, leveraged appropriately, hedged just so. For eighteen months I did this full-time. No software architecture. No consulting. Just trading.

I once made paper gains of 6 figures in a single day.

I also blew the whole thing up!!!!!! Hence I crawled back to the land of C# development!!

I’ll tell that story properly another time. The relevant bit for now is this: the trades that actually built real money were not the Pine Script trades. They were two simple long-term positions, taken with high conviction, held for years, executed with almost no complexity.

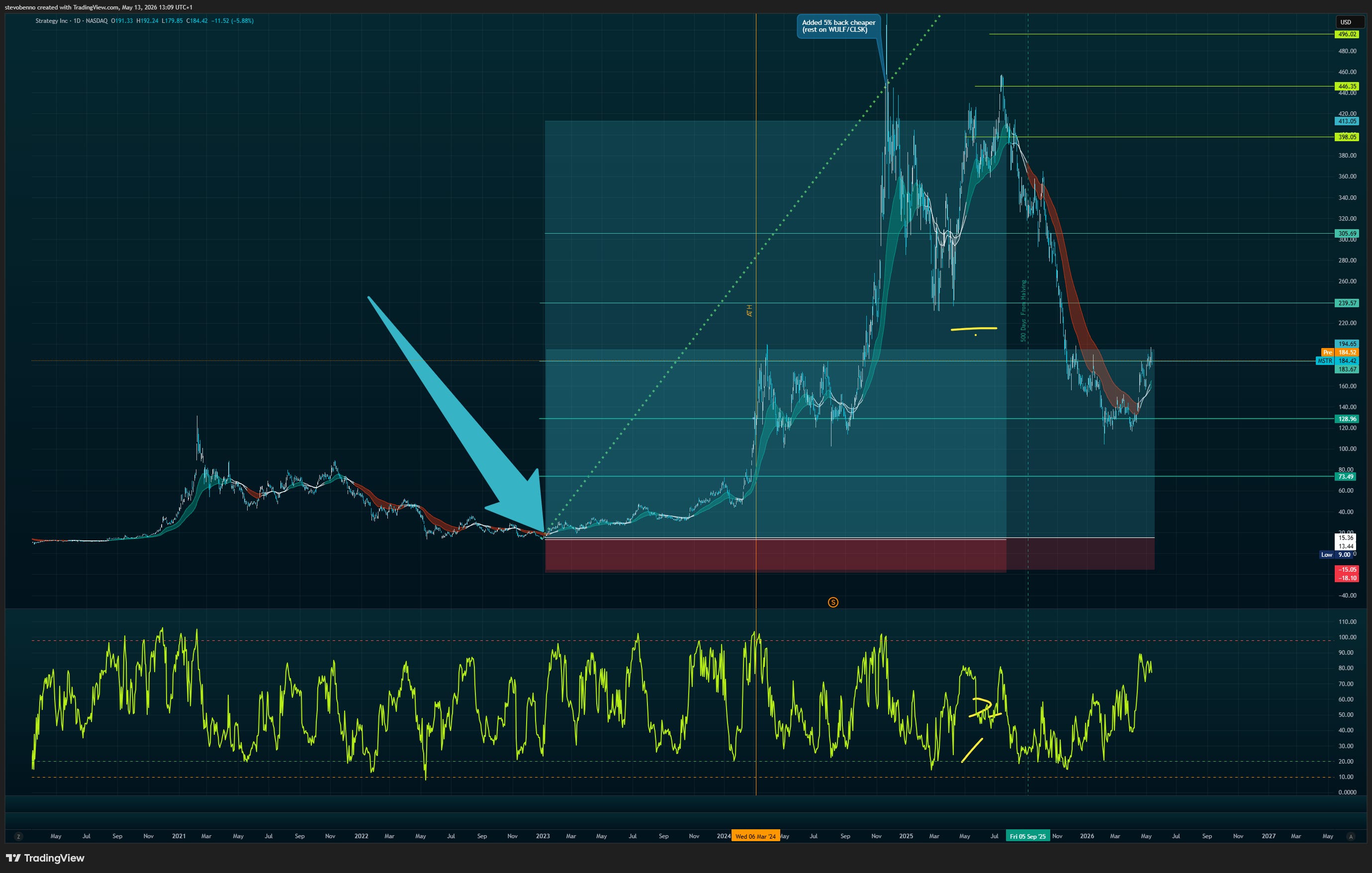

The first was Bitcoin via MicroStrategy at thirteen dollars in 2022.

The second was TeraWulf at a dollar in 2023.

Both produced roughly twenty-three times my money. Both required almost no active management. Both came from being directionally right about something most consensus opinion at the time was directionally wrong about. Neither required any of the elaborate instrumentation I’d spent years building.

This is not a coincidence. The relationship between thesis simplicity and outcome durability is, in my experience, almost monotonic. The cleaner the thesis, the better the trade. The more elaborate the structure required to express it, the more likely the structure itself becomes the failure point.

Which brings me to MicroStrategy now.

The original thesis

In 2022 the MicroStrategy thesis was beautiful in its simplicity. Saylor had decided to use the corporate treasury to buy Bitcoin. The company’s market capitalisation traded at a premium to the Bitcoin it held, which let him issue new equity at that premium and use the proceeds to buy more Bitcoin, which made each existing share back more Bitcoin than it had before. The flywheel was self-reinforcing as long as the premium held. Retail investors who could not easily buy Bitcoin directly, most institutional brokerage accounts, most retirement wrappers, most European retail platforms, could buy MSTR instead and get leveraged Bitcoin exposure through a NASDAQ-listed equity.

Saylor’s doctrine was straightforward. Never sell. Buy with every available capital instrument. Treat Bitcoin as the corporate treasury reserve asset. Twenty-one statements on the public record between 2020 and 2025, ranging from the corporate, “we will not sell”, to the personal, “sell a kidney before you sell your Bitcoin”.

The thesis worked because the doctrine was rigid. The flywheel worked because the premium was high. The premium was high because the doctrine was rigid. Each element reinforced the others.

I bought at thirteen dollars because the thesis was clear, the operator was credible, and the asymmetry was obvious. I held through every drawdown. I took twenty-five percent off at four hundred and twenty-eight dollars, which funded my facial feminisation surgery and several other things I needed money for. I kept the rest.

Then, on the fifth of May 2026, on the Q1 earnings call, Saylor said the company would sell Bitcoin to fund preferred share dividends.

In a single sentence, five years of doctrine evaporated.

The new architecture

The reason for the reversal is in the financial statements. Strategy posted a twelve and a half billion dollar net loss in Q1 2026, the third consecutive loss-making quarter. The mNAV premium that powered the original flywheel has compressed from a peak of around 2.6x to roughly 1.19x. Common stock has been diluted by three hundred and thirteen percent since 2020, the largest dilution of any ten-billion-dollar-plus US company by an order of magnitude. The next worst is Wayfair at thirty percent.

The flywheel stopped working because the premium stopped existing. Without a premium, new equity issuance is dilutive in Bitcoin-per-share terms rather than accretive. The original mechanism is structurally broken.

So Saylor invented a new one. Instead of issuing common equity against a premium that no longer exists, he is issuing perpetual preferred shares paying ten to eleven and a half percent dividends, using the proceeds to buy Bitcoin, and relying on Bitcoin’s long-term appreciation to outrun the dividend obligations. The instruments have names like Strike, Strife, Stride and Stretch, STRK, STRF, STRD, STRC, and a new euro-denominated Stream class called STRE. He calls this “Bitcoin yield” and frames the architecture as a three-layer capital stack of digital capital plus digital credit plus digital money.

Mathematically the model is self-sustaining if Bitcoin appreciates at more than about 2.3% annually. The marketing is sophisticated. The packaging is professional. The pitch is delivered with Saylor’s familiar evangelical confidence.

It is, structurally, a worse product than the one that existed before.

Not because the math is wrong. The math probably works in most scenarios. It is a worse product because it introduces fixed cash outflows that have to be funded regardless of Bitcoin’s price, because it inserts a layer of senior claimants ahead of common shareholders, because it depends on Bitcoin appreciating reliably enough to outrun the dividends, and because it replaces a simple thesis with a complicated capital stack. The old MSTR was “Bitcoin with leverage.” The new MSTR is “Bitcoin-backed structured credit with embedded volatility smoothing and preferred dividend obligations.” These are different products. The first one made me “richer”. The second one I have no particular interest in.

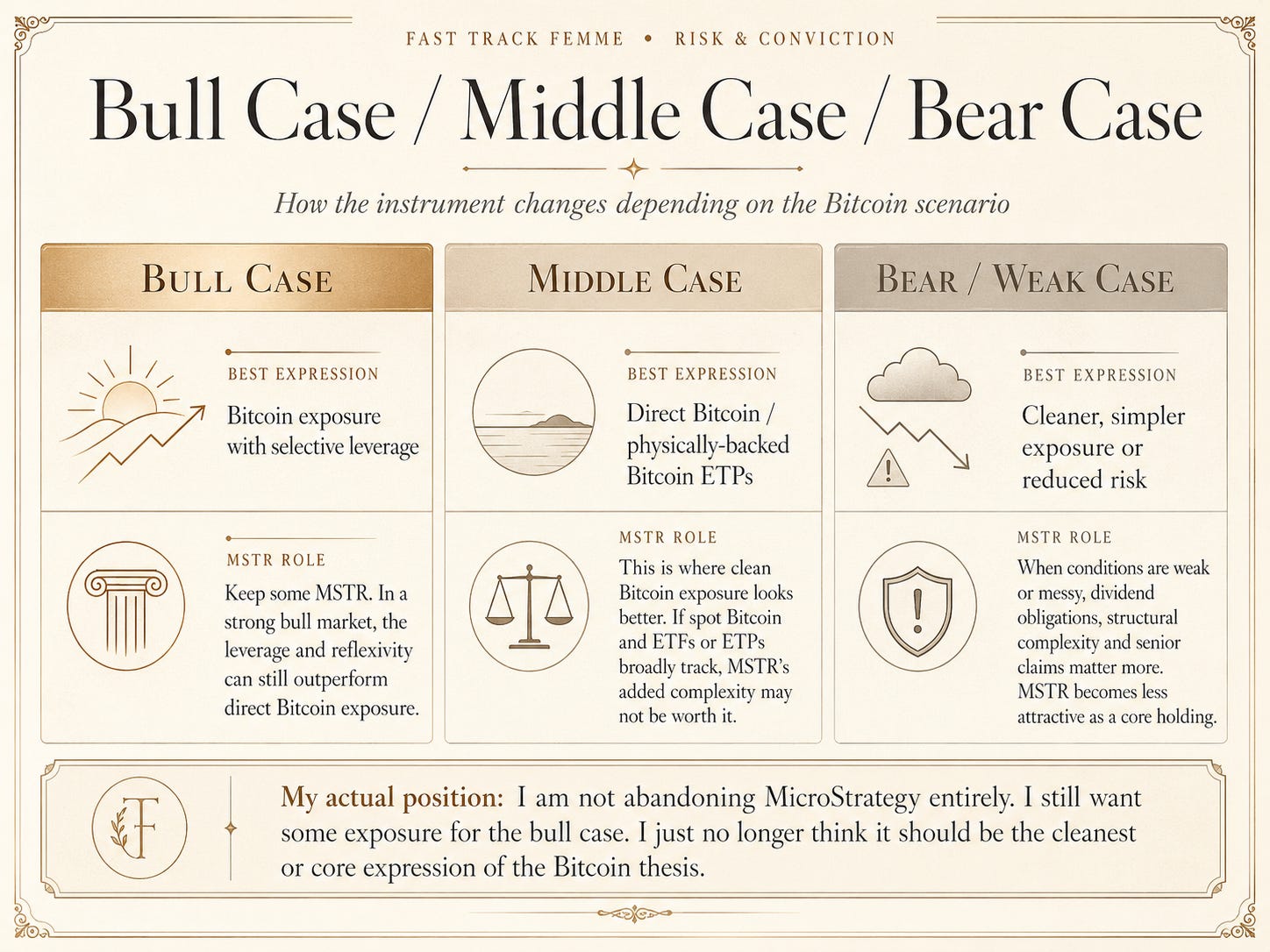

This is the meta-point. Being right about the underlying thesis does not mean staying with the original instrument. Bitcoin still goes up over a decade with volatility. That part of my thesis is intact. But the cleanest expression of that view is no longer MSTR. It is direct Bitcoin, or it is spot Bitcoin ETFs, or it is the new generation of physically-backed European Bitcoin ETPs. The instrument has become more complicated than the thesis requires. When that happens, the rational move is to step back to a cleaner instrument.

Which brings me to the European regulator

There is, of course, a problem.

The cleanest instruments for expressing the Bitcoin view are not always available to me. US-listed spot Bitcoin ETFs are mostly unavailable to European retail investors. The new Saylor preferred shares are unavailable too. European investor protection rules block retail investors from buying products that do not provide the correct European documentation, in theory to protect consumers from products they do not understand. In practice it means I can be blocked from buying instruments that are simpler, cleaner and better aligned with my actual thesis, while still being allowed to hold or sell more complicated positions I already own.

In my Irish pension account, I already hold MicroStrategy. I bought it early, held it through extraordinary volatility, and sold a slice near the highs. When it later fell sharply, I wanted to buy some back, and discovered I no longer could. I was allowed to sell the position, but not rebuild it.

So the position has become a one-way door. I am not being protected from risk. I am being prevented from choosing the cleaner version of a risk I already understand. And if I sell, I may not be able to replace it, which changes the psychology of the position completely.

So I have to work around it. Not by being clever. Not by building some baroque structure of my own. The opposite, actually. By simplifying.

What I am actually doing

The strategy I have settled on is straightforward and probably sensible.

Trim the WULF position further. The thesis has substantially played out, the price has run, the asymmetry that made the original trade interesting is largely gone. Keep a residual position because the AI infrastructure tailwind has further to run, but rotate the bulk of the gains into something cleaner.

Restructure the UK MSTR position partially. Rotate perhaps two-thirds of it into UK-listed physically-backed Bitcoin ETPs, the WisdomTree Physical Bitcoin product, or 21Shares Bitcoin Core. These are EU-compliant, retail-accessible, low-cost, and they express the underlying Bitcoin view without the structural overhead of Saylor’s yield architecture. Keep one-third in MSTR as a leveraged hedge for the bull case.

Leave the Irish MSTR position alone. The regulation has made the decision for me. It rides as a tax-free long-term hold inside the pension wrapper. The forced inability to trade it is, in this specific case, probably increasing my net wealth by preventing me from acting on impulses I might otherwise act on.

Deploy the dormant cash sitting in the Irish account into the same Bitcoin ETP, assuming the broker confirms availability inside the pension structure. The tax-free compounding inside the wrapper is doing real work. Leaving it in cash is the worst possible use of that wrapper.

This is not exciting. It is not Pine Script. It is not running synthetic spreads or building API adapters or any of the other elaborate technical work I used to do. It is taking a long-held conviction, recognising that the original instrument no longer expresses it optimally, and quietly migrating to a cleaner expression of the same view.

Which is, in the end, what most good investing actually looks like. The exciting part is identifying the thesis. The unexciting part is the long patient hold. The boring part is the periodic restructuring when the instrument no longer fits the thesis.

The broader problem

And this is where the problem becomes bigger than MicroStrategy.

I know, intellectually, that I need to move away from being so heavily tilted towards Bitcoin, Bitcoin proxies, Bitcoin miners, Bitcoin-adjacent infrastructure, and all the other strange little gravitational bodies orbiting the same central sun.

I know that.

The difficulty is that everything else looks expensive. US equities look expensive. AI infrastructure names look expensive. The obvious compounders look expensive. The safe things look boring. The interesting things look crowded. And the things that are not crowded are usually not crowded for reasons I discover about ten minutes after looking at them.

So I keep coming back to the same test.

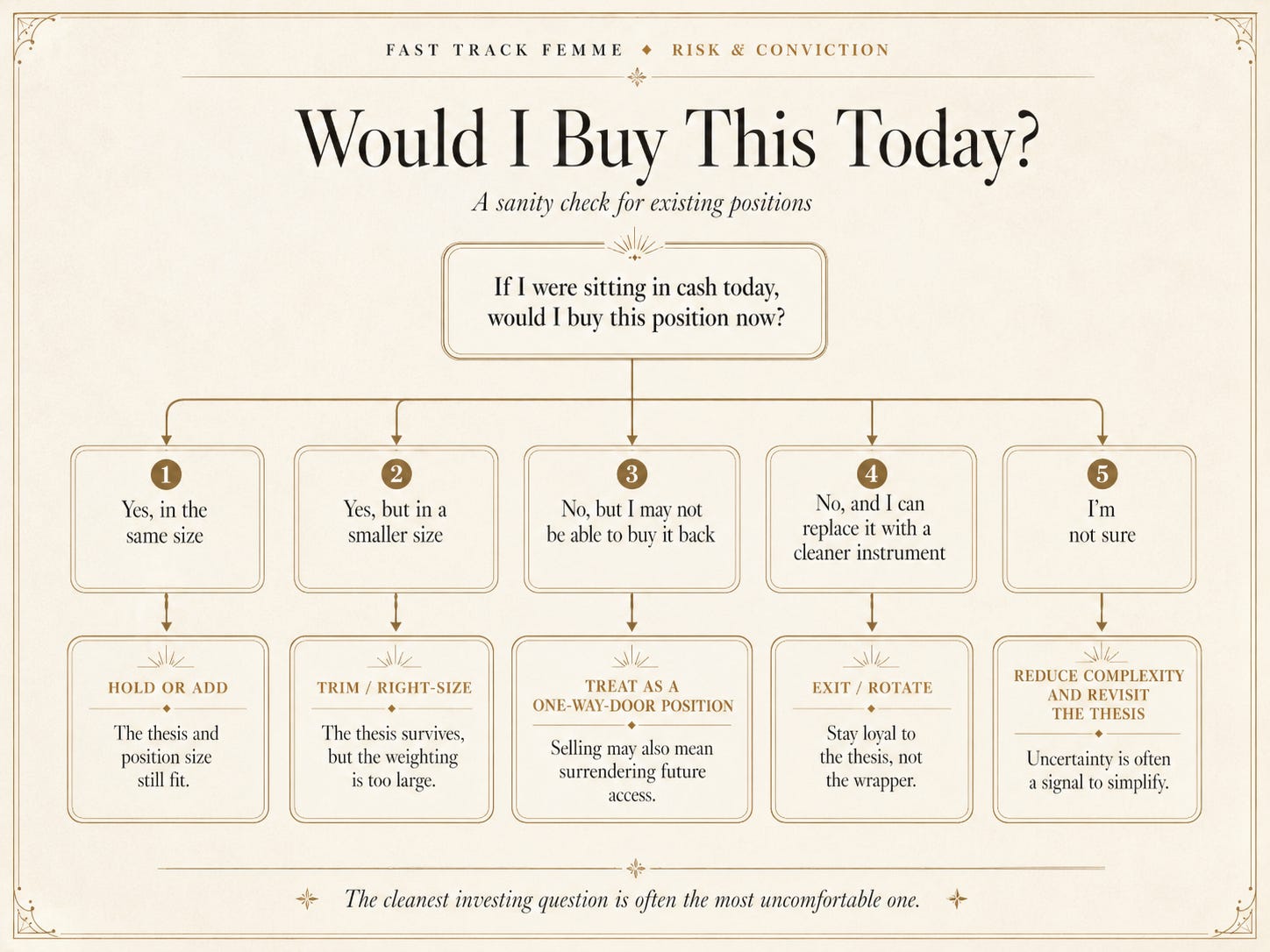

If I did not already own this today, would I buy it today?

That is the only question that really matters. Not whether I once had a good thesis. Not whether the trade worked. Not whether I am emotionally attached to the position because it paid for half the reconstruction of my head. If I were sitting in cash today, with no history, no attachment, no sunk cost, no victory lap, would I buy this thing now?

With WULF, the answer is probably: not in the same size.

With MSTR, the answer is: partly, but not as the cleanest expression of the Bitcoin thesis anymore.

With direct Bitcoin or physically-backed Bitcoin ETPs, the answer is still: yes, probably.

But the annoying complication is that my Irish position does not quite fit this clean little philosophical test. Because if I sell it, I may not be able to buy it back. That changes the decision. It turns the position into something closer to a one-way valve. I am not just asking, “Would I buy this today?” I am asking, “Would I give up the right to own this inside this wrapper, possibly forever?”

That is a different question.

And then there is the more human problem, which is that I understand this world. I understand Bitcoin. I understand the reflexivity. I understand the cultishness, the capital flows, the balance sheet games, the miners, the treasury companies, the volatility, the stupidity, the mania, and the opportunity buried somewhere underneath all of it.

I do not have that same edge in healthcare, industrials, consumer staples, biotech, banks, Japan, emerging markets, or whatever else I am supposed to rotate into like a sensible adult with a Morningstar subscription.

So yes, I probably need to broaden out.

But broadening out is not the same as blindly buying things I do not understand just because my current concentration makes me uncomfortable. Diversification is sensible. Diworsification is not. The fact that I am overexposed to one area does not automatically make every other area attractive.

That is the real problem now.

The trade worked. The instrument changed. The regulation interfered. The thesis survived, but its cleanest expression moved. And I am left with the most irritating investing question of all: not “Was I right?” but “What do I do next, now that being right is no longer enough?”

The trade that made me rich is now a trade I am not legally allowed to make. The regulator has decided I need protecting from products I understand. Saylor has decided to make his products too complicated for me to want anyway. Either way, the era is over.

The next thesis will come along, and when it does, the lesson is the same. Keep it simple. Hold it long. Ask whether you would buy it again today. Do not confuse loyalty to a position with loyalty to a thesis. And whatever you do, do not build forty different Pine Script indicators to confirm what you already know.